Successfully Complying with Lease Accounting Standard ASC 842

Introduction

One important area from Record-to-Report that is often overlooked during the consolidation of core functions is that of Lease Accounting, which became more complex with the release of ASC 842 which went into effect at the end of 2018. During a recent Peeriosity PeercastTM, the featured company shared their recent experiences with this type of transition, with emphasis on the challenges faced and the lessons learned during the project.

Company Experience

When the new lease standard, ASC 842 which requires leases to be recorded on the balance sheet and also requires enhanced disclosures within financial statements, was issued in February of 2016, a Peeriosity member company with $15 billion in revenue, decided that it would be a good time to not only make the changes to comply with this important accounting standard but also carry out consolidation and standardization of the entire Lease Accounting process. With an existing Global Business Services organization in place, with sites in every major geographic region, their site in Poland was selected to be the primary location for Lease Accounting activities.

The project was kicked off in September 2017 and continued in a phased approach until March 2019. The objectives of the consolidation project were as follows:

- Develop process design and standards according to new accounting requirements

- Deploy the new process standards globally (including Lease Maintenance application)

- Set up a centralized team to manage lease activities (input lease into software, validate the accuracy of input, prepare JE and reporting) for all entities in scope in one GBS Team

- Build GBS Team capabilities and set up proper infrastructure to support effectively new processes and standards

- Ensure all leases are fully reflected in the software by the end of 2018 and properly reported starting in 2019

One of the critical aspects of the consolidation project was the implementation of the CoStar Lease Accounting system, an advanced third-party solution. This system went live in March of 2018 and was then implemented in the various geographic regions in a phased approach over the next few months.

A wealth of additional details, including a view of the entire lease process, are available on the Peeriosity member website.

iPollingTM Results Review

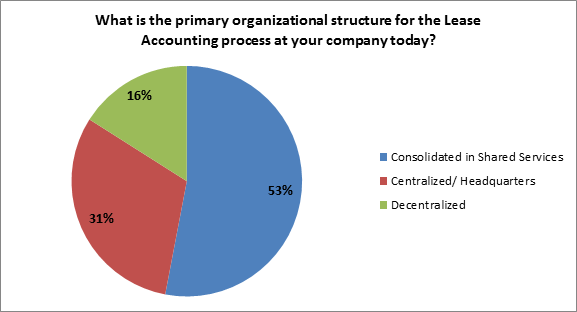

A poll related to Lease Accounting was recently created using Peeriosity’s iPollingTM technology and the results provide some good context in understanding where companies perform this function from both an organizational and geographic perspective. Looking first at what is the primary organizational structure for the Lease Accounting process, 53% of responding companies indicated that it is consolidated in Shared Services. Having this process as part of a centralized/headquarters function is how 31% of the companies are structured, with the remaining 16% utilizing a decentralized model.

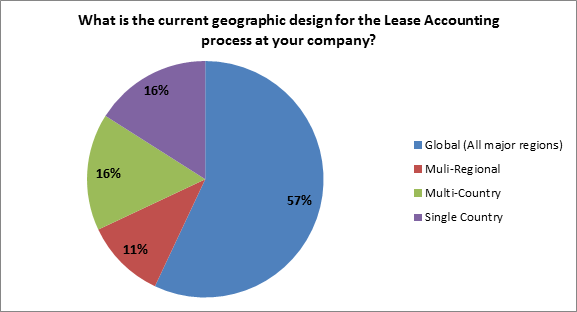

The second poll question then asked about the current geographic design for the Lease Accounting process. The results are interesting, with the global design being the most prevalent response at 57%. This was followed by multi-country and single-country both at 16%, and multi-regional at 11%.

Closing Summary

Depending on the company, the Lease Accounting process can be quite significant and complex, but its inherent transactional nature still makes it a great candidate to be consolidated into a Shared Services operation. When combined with the implementation of powerful technology and a concerted effort towards process improvement and standardization, the results can be significant.

What is the status at your company regarding the Lease Accounting process and compliance with ASC 842? Is your current approach providing the results you need or is it time to take another look at this important process area?

Who are your peers and how are you collaborating with them?

_____________________________________________________________________________

“PeercastsTM” are private, professionally facilitated webcasts that feature leading member company experiences on specific topics as a catalyst for broader discussion. Access is available exclusively to Peeriosity member company employees, with consultants or vendors prohibited from attending or accessing discussion content. Members can see who is registered to attend in advance, with discussion recordings, supporting polls, and presentation materials online and available whenever convenient for the member. Using Peeriosity’s integrated email system, Peer MailTM, attendees can easily communicate at any time with other attending peers by selecting them from the list of registered attendees.

“iPollingTM” is available exclusively to Peeriosity member company employees, with consultants or vendors prohibited from participating or accessing content. Members have full visibility of all respondents and their comments. Using Peeriosity’s integrated email system, Peer MailTM, members can easily communicate at any time with others who participated in iPollingTM.

Peeriosity members are invited to log into www.peeriosity.com to join the discussion and connect with Peers. Membership is for practitioners only, with no consultants or vendors permitted. To learn more about Peeriosity, click here.